What are lenders learning after losing $200 million a quarter?

SBA lenders have been working through unprecedented portfolio losses and asking real questions like “Should I be underwriting to a 15% decline?” That’s not a theoretical question – similar sentiments came up time and again from active franchise lenders.

Simply said, franchisors and franchisees are under stress and it is inadvertently affecting the lender experience. Lenders experienced unprecedented losses and are working through their portfolios. The content in this newsletter reflects firsthand feedback we got on how lenders are digesting those losses, what they’ve learned, and what it means for franchisors right now.

Below are some of the key insights important for franchisors to know – straight from some of the top franchise lenders in the US along with some positive developments for the SBA program overall.

Lenders experienced unprecedented losses. Now they’re changing how they lend.

The SBA franchise lending portfolio has gone through a period of significant stress. The losses were real — lenders were absorbing $200 million a quarter at peak — and the industry is now working through the consequences. Every tightening measure, every new line of scrutiny, every harder question franchisors are hearing from lenders right now flows from this moment. Understanding that context is the starting point for everything else in this newsletter.

At NAGGL, lenders were asking each other a question that should be on every franchisor’s radar: should we be underwriting to a sustained 15% profit margin decline? That’s not a theoretical question. It came from active franchise lenders, in the room, talking about what they’re seeing in their portfolios.

WHAT LENDERS HAVE LEARNED — AND WHAT IT MEANS FOR YOUR BRAND

Inflated startup costs are a leading cause of failure

Cost overruns at startup have become one of the clearest catalysts for franchise loan failures — because borrowers can’t catch up on liquidity once they fall behind. Lenders are now reading Item 7 line by line. One example that surfaced at the conference: a lender walked away from a home services deal because the franchisor required a vehicle costing nearly three times the price of a comparable used alternative. This was a sub-$350K loan. If lenders think your startup cost structure is inflated, they will back away — even on small deals.

Your system’s default history follows your brand everywhere

Lenders talk — and they carry their experiences with them when they move institutions. When a franchise system generates too many defaults, that reputation travels. Multiple brands across roofing, services, and kids services, car washes and healthcare came up by name at NAGGL. The answer to “will our system get a bad reputation if we have too many defaults?” is emphatically yes. There is no reset button.

How you manage distressed transfers shapes how lenders see your whole system

Workout specialists flagged a pattern franchisors should take seriously: when a franchisor controls a transfer process in a way that significantly undervalues the going concern of the business, it can leave lenders holding loans with inadequate collateral. This isn’t just a lender problem — it’s a reputation problem. How your brand handles distressed situations shapes how lenders underwrite every future deal in your system.

Sub-$500K deals are underserved — and there’s a reason

Smaller deal sizes continue to be passed over, and the reason goes deeper than lender capacity. The losses in the SBA franchise portfolio are concentrated in two areas: emerging brands and sub-$500K deals. This is a credit risk issue, not just an efficiency one. For franchisors with candidates in this range, understanding that lenders are underwriting to a higher risk bar — and preparing candidates accordingly — is essential.

Home services franchisors face two distinct challenges

First, the licensing catch-22: several significant franchise lenders will not extend financing until the business has its license in hand. In home services, equipment sometimes needs to be purchased before a license is issued — and in some states and trades, licensing backlogs run six months or longer. The franchisee ends up in a holding pattern. Second, lenders are asking a harder question about value: why would a consumer pay for a franchised home service when they could get a referral from a neighbor? Be prepared to articulate what your brand delivers that a standalone operator can’t. Lenders are asking — and so are borrowers.

THE BRIGHT SPOTS

SBA loan limits may be heading to $10 million

NAGGL officially announced on stage that they are advocating for an increase in the SBA loan limit from $5M to $10M. The SBA administrator herself noted that on an inflation-adjusted basis, the limit should already be at $7.5M. For franchisors in capital-intensive categories — childcare, hospitality, medical — this is meaningful.

Medical model: SBA policy is not changing

RELIEF FOR MEDICAL FRANCHISE BRANDS:SBA will NOT be changing its policy for medical franchises. After nearly a year of uncertainty, this is welcome news for the many brands that have been in limbo waiting for clarity.

Note: Some lenders will still require the medical provider as a personal guarantor before approving a deal — a hurdle worth anticipating and preparing candidates for if you operate in this space.

The FUND Score matters differently for start-ups vs. acquisitions

Lenders are willing to consider a lower FUND Score — FRANdata’s franchise credit score — for acquisition financing, which carries a lower risk threshold than start-up lending. For franchisors whose growth model relies heavily on new unit opens, this distinction is worth building into how you prepare candidates for the financing conversation.

The secondary market is holding — and that keeps lenders in the game

Despite rising early payment defaults and significant portfolio losses, the secondary market for the guaranteed portion of SBA loans remains active and pricing has stayed resilient. This is the liquidity and profit engine that keeps lenders willing to grow SBA programs. Worth monitoring as rates evolve, but for now it’s a genuine positive.

New lenders are entering the SBA market

A number of previously dormant SBLC licenses are being transferred to larger organizations, and more will be issued next year. This could meaningfully shift loan volume in the latter half of 2026 and into 2027. Names to watch now: Lafayette Square, NBH Bank, and OptimumBank. New entrants are ambitious — targets of $50–100M in year one — but still building their franchise pipelines. Contact FRANdata if you’d like to know more about connecting with these lenders.

The Franchise Directory deadline is June 30. It is not moving.

IF YOU’RE A FRANCHISE REGISTRY MEMBER WITH FRANDATA — YOU’RE COVERED

All of your certifications have been submitted, matched against the directory, and are being tracked with SBA. You do not need to worry about the deadline.

If your brand is not yet recertified on the SBA Franchise Directory by June 30, it will be delisted — and SBA lenders cannot approve loans for your franchisees until you’re back on it. Lenders are already front-running this: at least one major SBA lender is now prioritizing applications for brands not yet recertified, specifically to pull a PLP loan number before the window closes.

Not yet certified? Contact FRANdata now. Don’t let a certification gap stall your franchisees’ deals.

Lenders are recalibrating. Franchisors need to recalibrate with them.

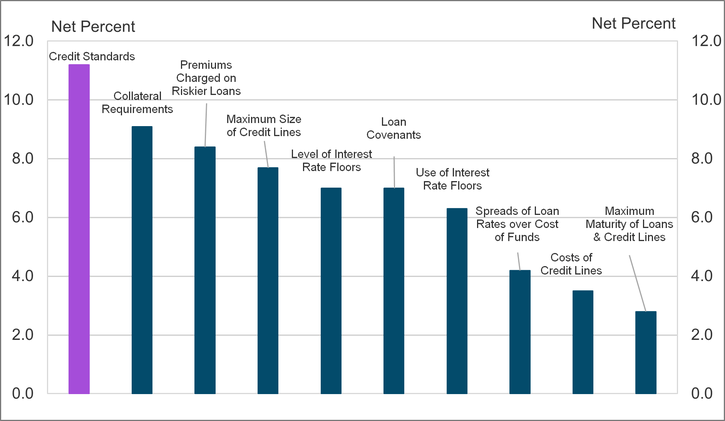

Lenders Continue to Tighten Credit Standards

Across virtually every dimension of commercial lending or SBA lending, banks are pulling back, and franchisors need to take note. The signal is consistent(refer to chart): net positive readings across all categories mean lenders are broadly making credit harder to access. Credit standards (purple bar) lead the tightening trend, with collateral requirements and premiums on riskier loans close behind — meaning franchisors and their prospective franchisees face higher bars for approval and steeper costs when risk is perceived. For franchisors evaluating system growth, this environment means franchisee candidates who looked financially qualified six months ago may no longer clear lender thresholds — making tools like FRANdata’s FUND Score or the Bank Credit Report more critical than ever for demonstrating creditworthiness to a more cautious lending community, we created these underwriting tools to bridge the gap between lenders and franchisors .

Source: Small Business Lending Survey

The SBA lending environment in 2026 is being shaped by hard lessons from portfolio losses. Lenders are tightening credit standards, scrutinizing startup costs, asking harder questions about brand value, and re-examining what they’ll finance and at what threshold. The franchisors who will move through this environment most effectively are the ones who understand what lenders have been through — and who prepare their systems and their candidates accordingly.

Questions about your brand’s lending profile or Directory status?

FRANdata works with franchisors, lenders, and PE firms to navigate SBA compliance and franchise credit intelligence. Contact us now