In the world of franchise funding, there’s a critical difference between eligibility and creditworthiness. As SBA lending policies tighten again, franchisors need to understand not just how to get listed—but how to get funded.

The SBA Franchise Directory and FRANdata’s Franchise Registry, they may sound similar, but they serve very different purposes for lenders.

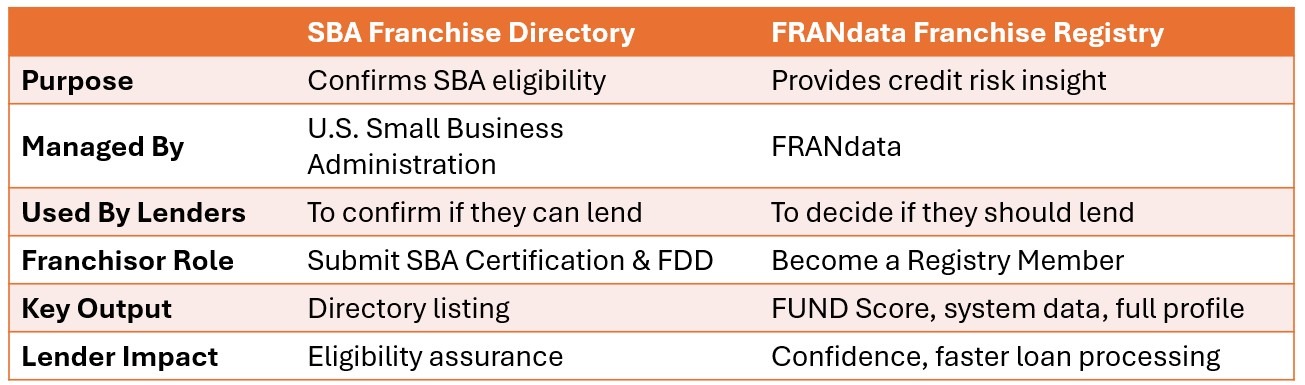

Franchise Directory: Tells Lenders They Can Lend

The SBA Franchise Directory is a list managed by the U.S. Small Business Administration. Its role is simple: it confirms that a franchise brand is eligible for SBA financing under the agency’s rules.

That eligibility is determined by a review of the franchise agreement and a signed Franchisor Certification—verifying things like transfer rights, ownership structure, and management roles. If the SBA deems your business model compliant, your brand is added to the Directory.

This tells lenders: you are allowed to make an SBA loan to this brand.

Franchise Registry: Tells Lenders They Should Lend

The Franchise Registry, operated by FRANdata, is used by over 9,000 lenders across the country. These lenders log in daily to access detailed information about franchise brands—not just whether they’re SBA-eligible, but whether they’re a sound credit risk.

FRANdata provides credit risk ratings (FUND Scores), to lender subscribers, on every franchise system with more than 50 units or 5 years in business. Newer brands receive an Emerging Credit Assessment that gives lenders early-stage risk guidance (green/yellow/red light).

“The Franchise Directory says lenders can lend. The Franchise Registry tells them whether they should,” said Edith Wiseman, President at FRANdata

And this isn’t theoretical—more than 60% of all SBA franchise loans are financed by banks that rely on FRANdata’s FUND (Franchise Credit Scoring) Report for underwriting. That makes the Registry not just a useful resource, but a central part of the franchise loan approval process.

Who at the Bank Uses the Registry—and Why It Matters

One of the most overlooked facts: it’s not just one “lender” making the call. Franchise loans are influenced by multiple people across a lending institution—and each of them uses the Franchise Registry differently.

Here’s a breakdown of who accesses the Registry:

- Business Development Officers (BDOs): Use it to identify eligible and fundable brands before engaging borrowers.

- Underwriters: Use it to validate credit risk and guide structuring decisions.

- Credit Committees/Decision-Makers: Rely on the Registry for independent third-party data that supports their approval decisions.

- Closers & Servicers: Refer to it to ensure all eligibility documentation is in place.

- Special Assets & Portfolio Managers: Review it to evaluate brand performance across the lender’s portfolio and adjust internal lending policies.

“A portfolio manager might say: we’re not doing any loans under a 650 score—so they’re using the Registry to filter brands based on our FUND Score,” Edith explained. “Even workout and servicing teams rely on our data when franchise loans go bad.”

Download the Franchise Registry lender reach overview (PDF)