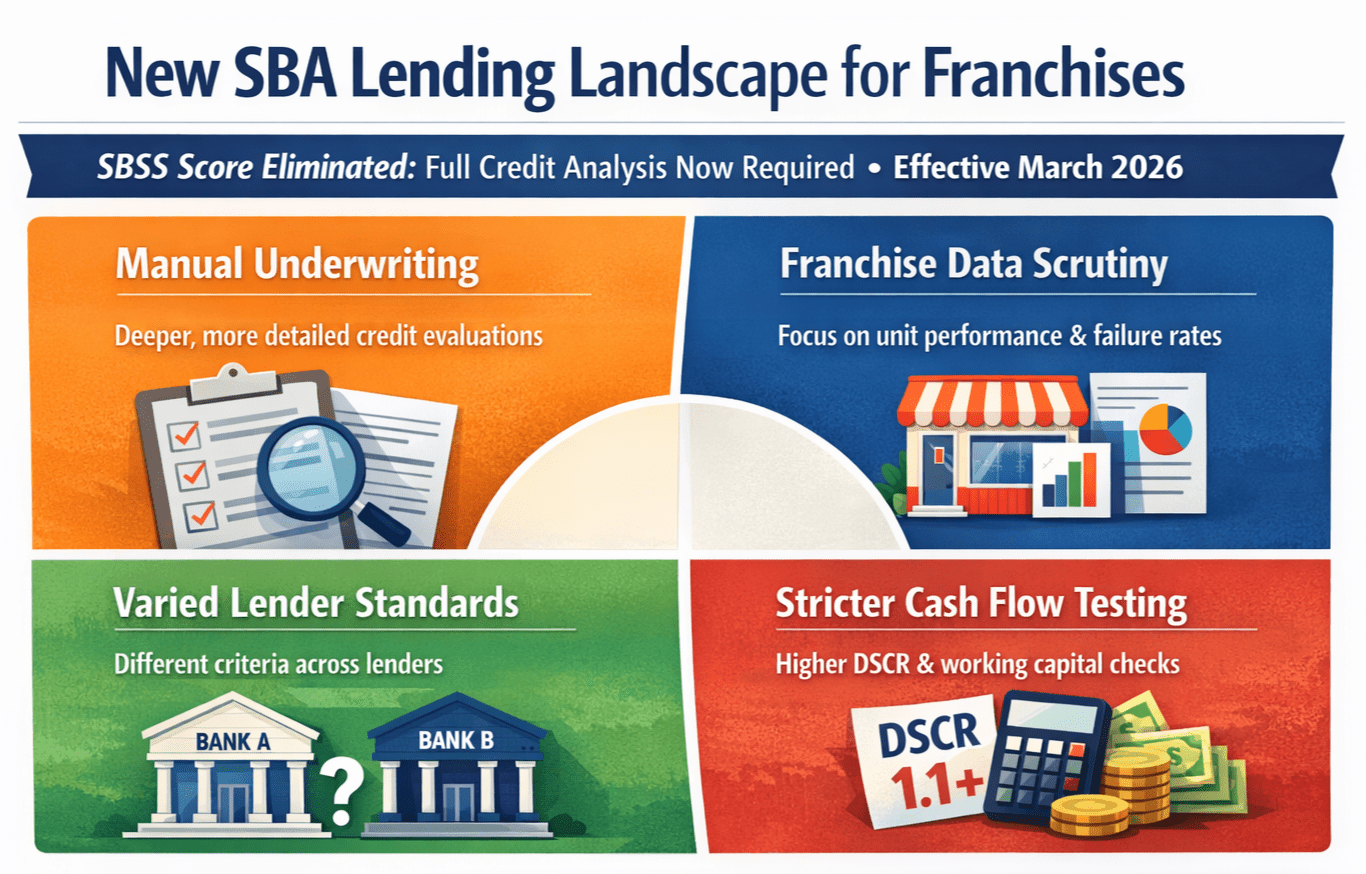

The Small Business Administration has formally announced that the FICO Small Business Scoring Service (SBSS) Score will no longer be used for 7(a) Small Loans beginning March 1, 2026. This policy change has significant SBA SBSS sunset franchise financing implications for franchisors as lenders shift toward new underwriting requirements.

The Small Business Administration has formally announced that the FICO Small Business Scoring Service (SBSS) Score will no longer be used for 7(a) Small Loans beginning March 1, 2026. This policy change has significant SBA SBSS sunset franchise financing implications for franchisors as lenders shift toward new underwriting requirements.

For franchisors, the end of SBSS scoring marks a meaningful change in how lenders evaluate franchise loan requests—and it will directly affect how easily prospective and existing franchisees can secure SBA financing.

What’s Changing?

For years, the SBSS score provided a standardized, automated way for lenders to assess credit risk on smaller 7(a) loans. With the SBSS sunset, the main SBA SBSS sunset franchise financing implications include:

-

Lenders must now rely on full credit analysis rather than automated scoring.

-

SBA’s new procedures focus on traditional commercial credit evaluation.

-

Lenders may use internal business credit models if they meet regulatory standards.

-

SBA Express loans are not affected.

The industry is moving away from a score-driven baseline and toward a more individualized, documentation-heavy process.

Why This Matters for Franchisors

More Traditional, Manual Underwriting

The SBSS sunset requires lenders to conduct deeper, more detailed credit reviews. Borrower financials, credit history, projected cash flow, collateral, guarantors, and repayment ability will all receive closer scrutiny. This is one of the most immediate SBA SBSS sunset franchise financing implications for franchise development and deal timelines.

Franchise Performance Data Becomes More Critical

Under the updated rules, lenders must evaluate franchise-specific information such as:

-

the number of failed franchisees

-

system cash-flow projections

-

unit performance indicators

-

relevant management or operational structures

This shift makes franchise transparency essential and creates additional SBA SBSS sunset franchise financing implications for how franchisors support lenders and franchisees.

Increased Variability Across Lenders

Without a universal scoring threshold, lenders will rely on their own credit models and franchise familiarity. This creates more variability in credit decisions. Understanding this variability is key for navigating SBA SBSS sunset franchise financing implications, especially when franchisees work with multiple lenders.

Strong Financial Modeling & Cash-Flow Support Are Essential

Lenders must now analyze DSCR, cash-flow strength, bank activity, and working capital justification. SBA requires a DSCR of 1.1:1 or greater. Strong, defensible financial modeling becomes central to handling SBA SBSS sunset franchise financing implications in a more rigorous underwriting environment.

What Franchisors Should Do Next

1. Review and strengthen your system’s economic data.

Ensure unit-level economics, performance trends, and system stability metrics are current, accurate, and easy for lenders to assess.

2. Provide lender-friendly documentation to franchisees.

Templates, projections, and standardized financial tools will help franchisees present complete, lender-ready packages that meet the expectations created by SBA SBSS sunset franchise financing implications.

3. Engage your preferred lenders early.

Discuss how their internal credit models will change and what new underwriting expectations look like without SBSS in place.

4. Educate franchisees on the new requirements.

Help franchisees understand the heightened importance of cash-flow support, DSCR strength, and comprehensive documentation.

5. Leverage your Franchise Registry membership to increase lender confidence.

Membership ensures your brand’s information is verified, centralized, and easily accessible to lenders—reducing friction and helping mitigate SBA SBSS sunset franchise financing implications. Registry members also benefit from tools like FUND Score & Report (for systems with 50+ units) and consultations that connect system performance to lender expectations

6. Use the Franchise Registry membership to understand how lenders see your brand.

FRANdata’s Franchise Registry is used by more than 9,000 lenders across the country, many of whom rely on FRANdata’s FUND Score and related analytics when assessing franchise credit risk, setting terms, and making loan decisions. By maintaining an active membership, reviewing your FUND Score and report, and using FRANdata’s financing consultations, you gain visibility into the same information lenders are using. That perspective helps you refine how your opportunity is presented, address gaps or concerns before they show up in underwriting, and take control of how lenders evaluate your brand in a post-SBSS environment

Final Thought

The elimination of SBSS scoring is one of the most important shifts in SBA lending in years. Understanding the SBA SBSS sunset franchise financing implications and preparing proactively will help franchisors maintain strong capital-access pathways for their franchisees. Brands that invest in transparency, financial readiness, and lender communication now will be best positioned to thrive under the new SBA framework.

________________________________________________________________________________

FAQ: SBSS Sunset & Franchise Financing

1. What is the SBSS score and why is it going away?

The SBSS score was an automated credit-scoring tool used by lenders to pre-screen 7(a) Small Loans. Beginning March 1, 2026, SBA is discontinuing its use and requiring lenders to rely on more traditional credit analysis methods instead.

2. How will the SBSS sunset affect franchisee loan approvals?

Lenders will need more documentation, more financial detail, and stronger system-level data to approve franchise loans. Deals may take longer and require more support from franchisors.

3. Are all SBA loans affected?

No. SBA Express loans are not part of this change and may still use SBSS scoring. The new rules apply only to 7(a) Small Loans.

4. What type of information will lenders expect from franchisors now?

Lenders will look more closely at unit-level performance, historical cash-flow patterns, failed-unit counts, start-up cost accuracy, and system stability indicators.

5. How does the SBA SBSS sunset franchise financing implications impact emerging brands?

Emerging brands with limited performance history may face heightened scrutiny. Clear financial modeling and transparent economic assumptions will be essential to support franchisee financing.

6. Will lender requirements vary more now?

Yes. Without a standardized scoring threshold, lenders will use their own credit models and franchise experience, which can lead to different outcomes for similar applicants.

7. How does Franchise Registry membership help franchisors during this transition?

The Franchise Registry centralizes and verifies franchisor information for lenders, increasing confidence in the brand while reducing back-and-forth requests. It also helps franchisors understand how lenders view their system and what data may need strengthening.

8. What should franchisors prioritize first?

Strengthen your unit economics, verify your financial models, update your Franchise Registry profile, and proactively communicate with lenders about how your system supports franchisee repayment ability.